Media release on 1st quarter results 2015

PDF-version of this media release

Bernard Fontana, CEO, comments on the results: “Holcim reported robust development in the first quarter 2015, with an increase in financial performance despite a different weather pattern and some volume declines compared to a very strong previous year’s quarter. Holcim also generated higher cash flow from operating activities and increased net income significantly supported by the gain from the divestment of the Group’s minority shareholding in Siam City Cement.”

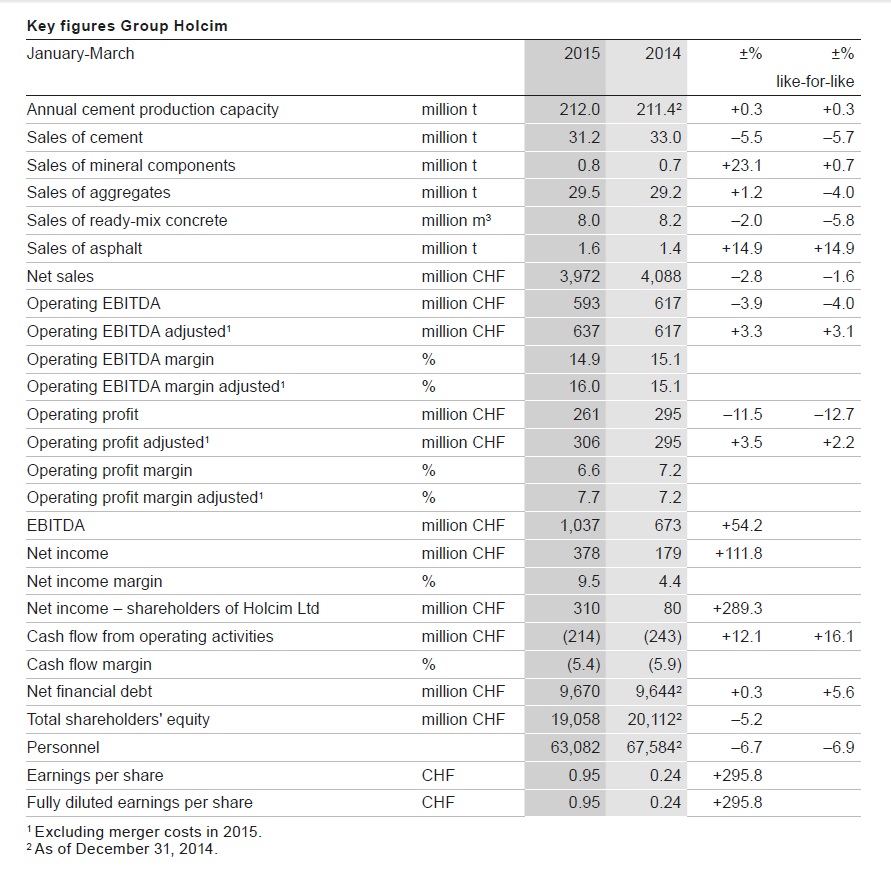

Holcim continued to operate in a weak global economic environment that was characterized by uncertainty and moderate growth prospects. The development was positively impacted by lower oil prices but at the same time investment weakness more than offset these effects in both advanced and emerging markets. However, based on its strong geographic footprint, focus on prices, disciplined cost management, and previous restructuring, Holcim was able to mitigate the adverse economic effects. Following the exceptionally strong first quarter 2014, cement deliveries declined as all Group regions except North America and Latin America sold less volume. However, in important markets including Mexico, the United States, and the Philippines more cement was sold. Aggregate shipments increased thanks to Holcim Germany, Aggregate Industries UK, and Aggregate Industries US. Ready-mix concrete volumes were down.

Adjusted for merger costs, operating EBITDA increased, mainly as a result of the positive development in the Group regions Asia Pacific and Latin America. Operating profit adjusted for merger costs was also higher. ACC in India, Holcim Spain, Holcim Australia, Aggregate Industries UK, and Holcim Mexico were the Group companies with the strongest progress, while countries such as France, Indonesia, Canada, and Lebanon reported lower financial results.

ROIC after taxes stood at 8.1 percent, while net financial debt decreased.

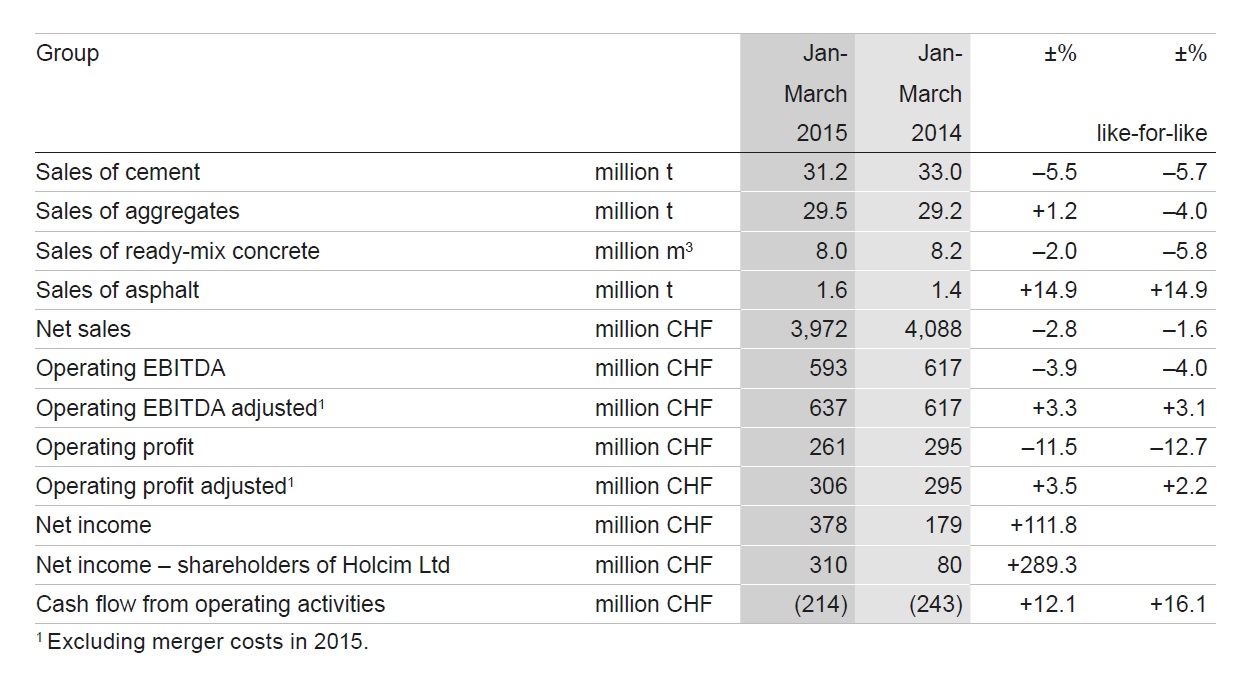

Holcim Group, January-March

Sales volumes

Consolidated cement volumes decreased 5.5 percent to 31.2 million tonnes in the first three months of the year. While North America and Latin America increased cement volumes, the other Group regions reported declines. Aggregates volumes increased 1.2 percent to 29.5 million tonnes, as the volume growth in Europe and North America was able to make up for the negative development in other Group regions. Ready-mix concrete deliveries reached 8.0 million cubic meters, a decline of 2.0 percent, which was mainly attributable to less favorable development in Latin America, where the focus remained on high-margin applications, and North America. Asphalt sales were up markedly by 14.9 percent to 1.6 million tonnes.

Cement prices increased 4.0 percent and aggregates prices 4.2 percent.

Financial results

Like-for-like net sales across the Group decreased 1.6 percent during the first quarter of the year. Reported net sales were down 2.8 percent to CHF 3,972 million, as increases in North America could not compensate for lower sales in other Group regions.

Operating EBITDA adjusted for merger costs of CHF 44 million was 3.3 percent higher than last year. The adjusted operating EBITDA margin increased to 16.0 percent. Reported operating EBITDA decreased 3.9 percent to CHF 593 million, impacted by merger costs and lower financial performance in the Group regions Europe and Africa Middle East. Operating profit adjusted for merger costs of CHF 44 million was up 3.5 percent, while the adjusted operating profit margin increased to 7.7 percent. Reported operating profit decreased by 11.5 percent to CHF 261 million, as increases in the Group regions Asia Pacific and Latin America were not able to compensate for merger costs and lower performance in Europe and in Canada, where a harsher winter was noted.

Net income increased significantly by 111.8 percent to CHF 378 million, mainly as a result of the divestment of Holcim’s minority shareholding in Siam City Cement. Net income attributable to shareholders of Holcim Ltd was also up markedly by 289.3 percent to CHF 310 million.

Cash flow from operating activities improved 12.1 percent to CHF -214 million in the first quarter, a quarter which is traditionally lower than the others. Net financial debt over the last twelve months decreased by CHF 370 million and stood at CHF 9,670 million.

Holcim Leadership Journey

In the first quarter of 2015, the contribution of the Holcim Leadership Journey to the Group’s operating profit amounted to CHF 85 million. The Customer Excellence Stream contributed CHF 21 million and the cost initiatives CHF 64 million to this result building on the good traction in the procurement and logistics streams.

Portfolio optimization

Holcim continued to actively optimize its operational footprint in the first quarter of the year. The Group sold its entire remaining shareholding of 27.5 percent in Siam City Cement in Thailand via a private placement in capital markets. For the sale of its entire remaining stake, Holcim received a total consideration of CHF 661 million, which resulted in a gain before taxes of CHF 371 million. Early in January 2015, Holcim also closed its series of transactions in Europe with Cemex.

On March 25, 2015 Holcim received from the Foreign Investment Promotion Board (FIPB) the approval for the planned simplification of the Group’s structure in India. The FIPB in turn has sent the case with a recommendation for approval to the Cabinet Committee of Foreign Affairs (CCEA). Holcim is now awaiting final approval by the CCEA in the coming weeks.

Merger to create LafargeHolcim

In March 2015 Holcim and Lafarge reached an agreement on revised terms for their merger, taking another important step forward towards becoming the most advanced company in their industry. The Boards of Directors of both companies agreed on a new exchange ratio of 9 Holcim shares for 10 Lafarge shares. Holcim and Lafarge have also agreed that, subject to shareholder approval, the new company will announce a post-closing scrip dividend of 1 LafargeHolcim share for each 20 existing shares.

Eric Olsen was appointed future Chief Executive Officer of LafargeHolcim, to take office as of the closing of the merger project. Eric Olsen is presently Lafarge Executive Vice-President Operations and has been a member of that Group’s Executive Committee since 2007. Wolfgang Reitzle will act as the statutory Chairman and Beat Hess will be Vice-Chairman of the Board. In addition, Wolfgang Reitzle and Bruno Lafont will be non-executive Co-Chairmen of the Board.

In February, Holcim and Lafarge announced that CRH plans to acquire the majority of the assets that were identified during the divestment process for an enterprise value of CHF 6.8 billion. These assets are mainly in Europe, Canada, Brazil, and the Philippines. Following these important milestones, both companies are continuing to work intensively on preparing the closing of the transaction and a successful post-merger integration.

Outlook for 2015

Holcim expects for 2015 that the global economy continues its gradual recovery. Key construction markets of Holcim in countries like the USA, India, Indonesia, Mexico, Colombia, the UK, and the Philippines are expected to be the main growth drivers. Europe overall should have a flat development. Latin America will continue to face uncertainties in countries such as Argentina and Brazil but should overall show slight growth in 2015. The Asia Pacific region is expected to grow although at a still modest pace. Africa Middle East is expected gradually to improve.

In this environment cement volumes should increase in all Group regions in 2015 with the exception of Europe. Aggregate and ready-mix concrete volumes are expected to increase. On a stand-alone basis and unconnected to the proposed merger with Lafarge, the Board of Directors and Executive Committee of Holcim expect like-for-like operating profit adjusted for merger-related costs to be between CHF 2.7 billion and 2.9 billion in 2015. Higher pricing and ongoing cost savings are anticipated to offset cost inflation, leading to a further expansion in operating margins in 2015.

Key figures per Group region

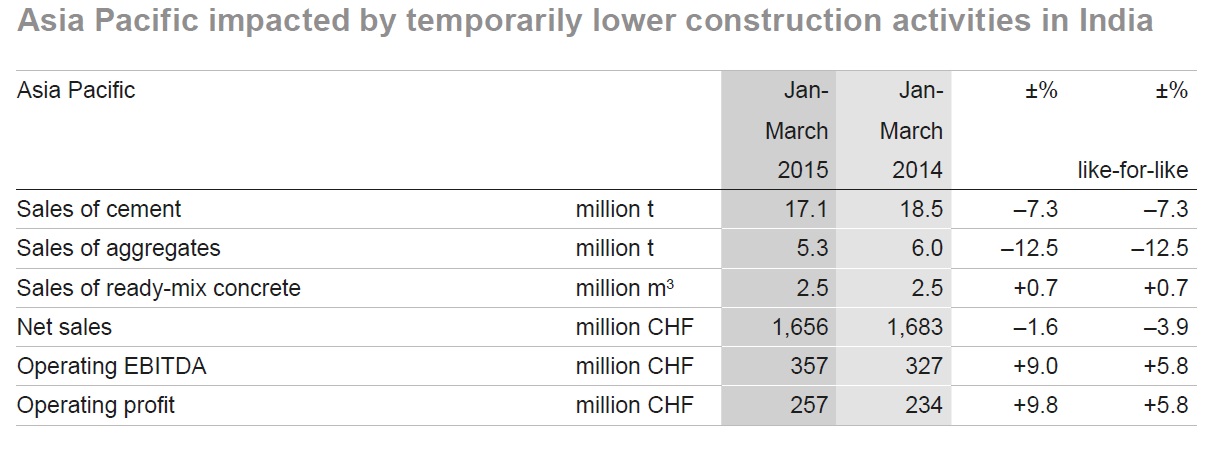

Asia Pacific impacted by temporarily lower construction activities in India

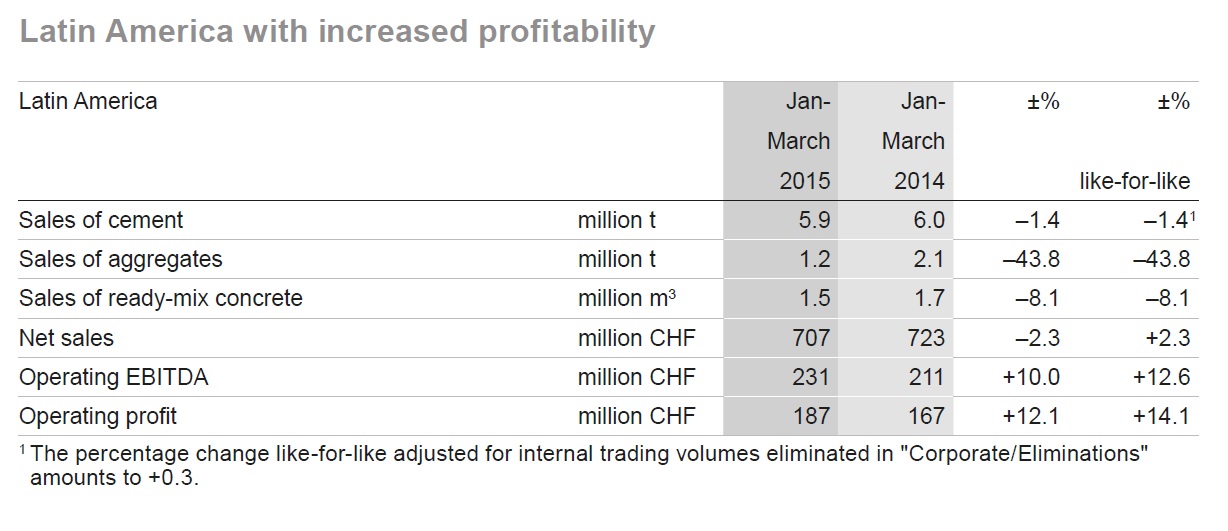

Latin America with increased profitability

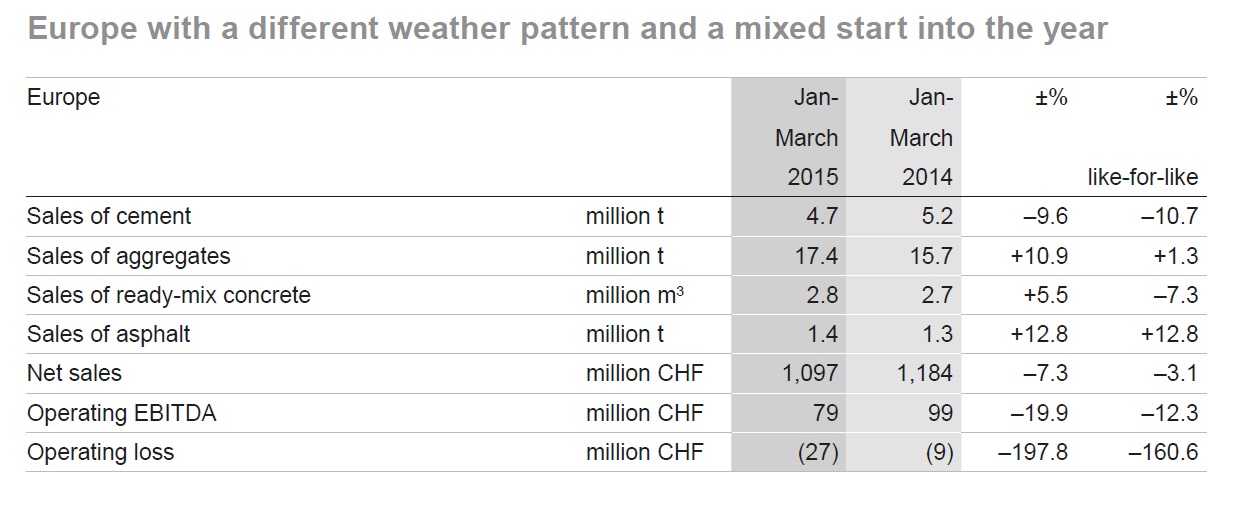

Europe with a different weather pattern and a mixed start into the year

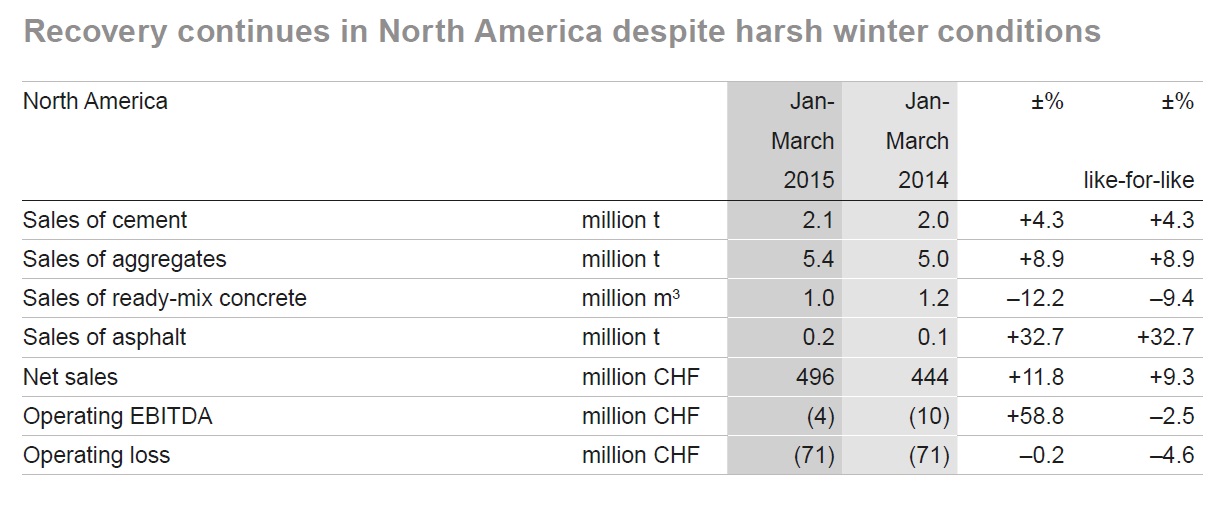

Recovery continues in North America despite harsh winter conditions

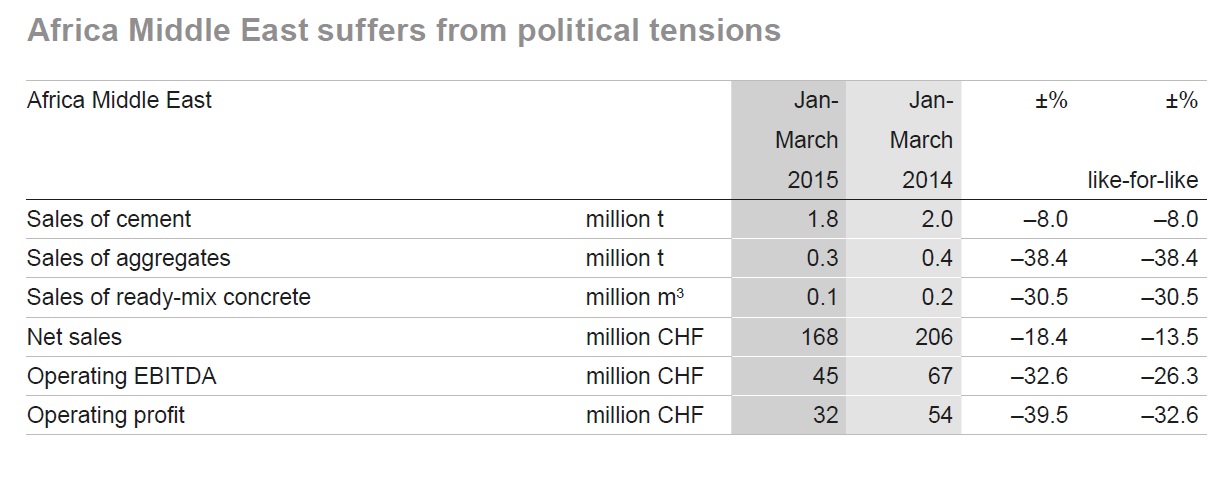

Africa Middle East suffers from political tensions

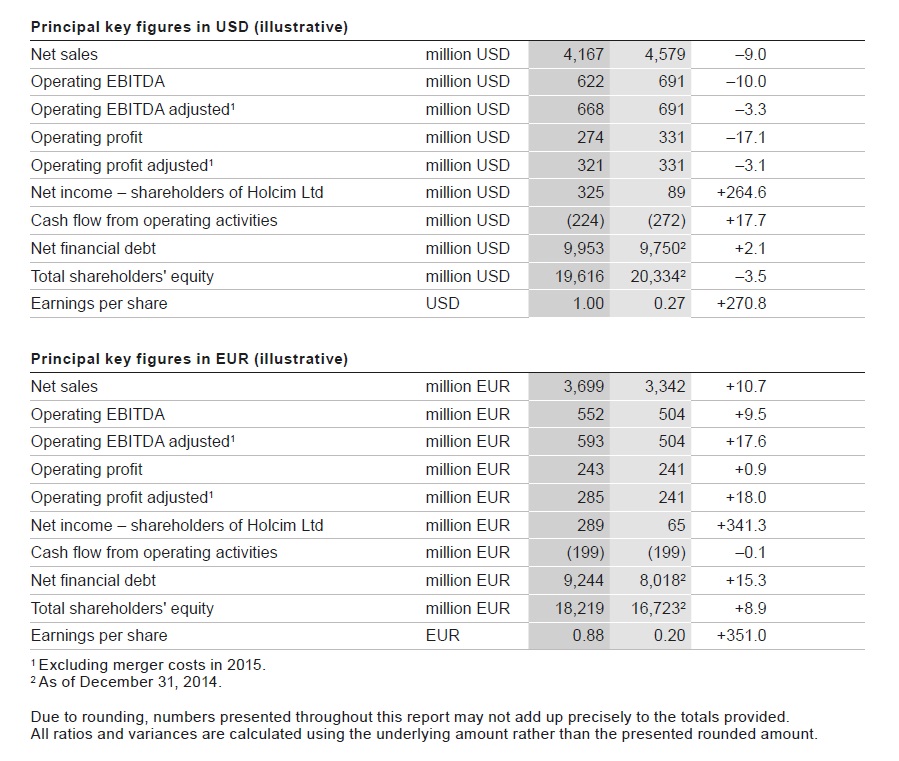

Principal key figures in USD/EUR (illustrative)

Additional information such as the First Quarter Interim Report 2015 including detailed information on the Group regions, is available at www.holcim.com/results

* * * * * * *

Holcim is one of the world's leading suppliers of cement and aggregates (crushed stone, gravel and sand) as well as further activities such as ready-mix concrete and asphalt including services. The Group holds majority and minority interests in around 70 countries on all continents.

* * * * * * *

This media release is also available in German at www.holcim.com/news.

* * * * * * *

Corporate Communications: Phone +41 58 858 87 10

Investor Relations: Phone +41 58 858 87 87

* * * * * * *

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}