Media release on 3rd quarter results 2014

- Les objectifs du Holcim Leadership Journey sont dépassés au troisième trimestre.

- Augmentation des volumes comparables de ciment entraînée par les progrès dans les régions de l'Asie Pacifique, de l'Amérique du Nord et du Moyen-Orient.

- Augmentation des ventes nettes comparables dans toutes les régions du groupe grâce à de plus grands volumes et des meilleurs prix.

- Augmentation du profit opérationnel malgré les coûts de la restructuration et de la fusion qui ont atteint 91 millions de francs suisses.

- L'effet négatif des devises diminue, mais continue cependant à peser sur la performance financière du groupe.

PDF-version of this media release

Bernard Fontana, CEO, comments on the results: “Holcim posted a solid like-for-like performance in the first nine months of 2014 building on the good traction earlier in the year and despite the ongoing challenging market environment. The Group increased like-for-like operating profit on the back of the solid financial performance in North America, Europe, and Africa Middle East. However, weak emerging market currencies continued to negatively impact consolidated financial performance, in particular in Asia Pacific and Latin America.”

While the recovery of the global economy continued during the course of 2014, overall the development was considerably weaker than expected. Many advanced economies were still confronted with high levels of public and private debt which continued to impact growth potential, while emerging markets were slowing down from pre-crisis growth rates. Holcim’s balanced geographic footprint once again proved to be an important strength that was able to partly mitigate the effects of uneven development across the different markets of the Group. The Group companies in the United States, India, the Philippines, Morocco, and Russia recorded significantly higher cement volumes, while Azerbaijan, Italy, Argentina, and Ecuador reported more pronounced volume decreases. Aggregates and ready-mix concrete volumes decreased mainly due to the business restructuring and divestments in Latin America last year.

Like-for-like operating EBITDA increased thanks to the Group companies in the United States, the United Kingdom, Ambuja Cements in India, and Russia. The increase in like-for-like operating profit was mainly supported by better financial performance in North America, and despite restructuring costs of CHF 37 million and merger costs of CHF 54 million. Like-for-like and adjusted for merger and restructuring costs, operating profit increased by CHF 141 million representing an increase of 7.8 percent. Operating profit margin adjusted for restructuring and merger costs was 12.7 percent and increased compared to the previous year.

The price development in several Group companies was positive as well, as Holcim was able to achieve more favorable price levels in key markets including India, Mexico, and the United States.

Compared to the first nine months of 2013 ROIC before taxes increased from 7.2 percent to 8.2 percent.

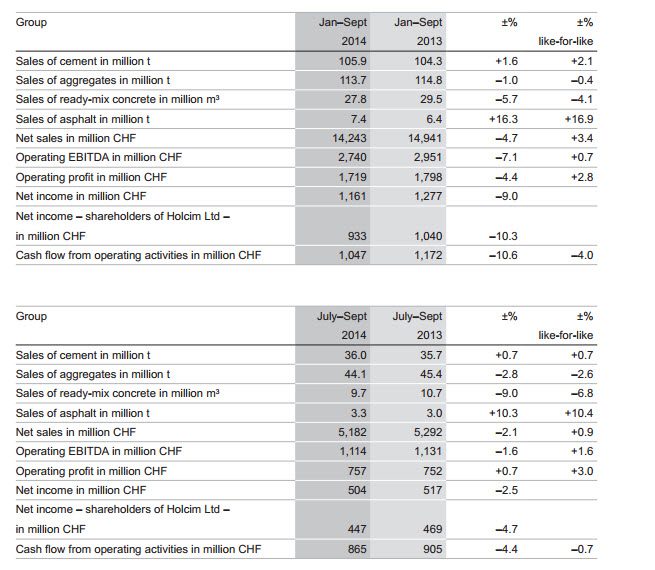

Holcim Group, January-September and July-September

{kind=link}

Sales volumes

Group-wide cement volumes increased 1.6 percent to 105.9 million tonnes over the first nine months of 2014 mainly driven by positive volume developments in the United States, India, and the Philippines which offset lower volumes in Azerbaijan, Italy, and Argentina. Aggregates volumes were down 1 percent to 113.7 million tonnes primarily as a result of the segment’s restructuring in Latin America, where a number of underperforming sites were closed or divested in 2013, and lower volumes in France. Ready-mix concrete volumes reached 27.8 million cubic meters and were 5.7 percent lower than 2013 mainly due to last year’s restructurings and divestments as well as market contraction in Group Region Latin America. Asphalt volumes increased 16.3 percent to 7.4 million tonnes.

Financial results

On a like-for-like basis, consolidated net sales were up 3.4 percent as a result of higher volumes and better pricing in many markets. Consolidated net sales for the Group decreased 4.7 percent to CHF 14.24 billion. Negative currency effects – mainly in Asia Pacific and Latin America – were the main contributor to this development, weighing on consolidated net sales by CHF 1.05 billion.

Like-for-like operating EBITDA increased 0.7 percent. Consolidated operating EBITDA was down 7.1 percent to CHF 2.74 billion mainly due to currency effects. Adjusted for restructuring and merger costs operating EBITDA was CHF 2.82 billion. North America and Europe, the two Group regions less affected by the significant currency effects, recorded a plus in operating EBITDA.

Operating profit reached CHF 1.72 billion, an increase of 2.8 percent on a like-for-like basis. Like-for-like and adjusted for merger and restructuring costs, operating profit increased by CHF 141 million, representing an increase of 7.8 percent.

Net income was down 9 percent to CHF 1.16 billion partly because Holcim has not yet received the final compensation installment of USD 97.5 million for the nationalization of Holcim Venezuela which was due on September 10, 2014. In addition, the Group benefited from the one-time gain from the sale of 25 percent in Cement Australia in 2013. Net income attributable to shareholders of Holcim Ltd declined by 10.3 percent to CHF 933 million.

Cash flow from operating activities was down 10.6 percent to CHF 1.05 billion compared to the same period in 2013 due to foreign exchange impacts and lower dividends received. Over the last twelve months net financial debt of the Group was CHF 10.41 billion, CHF 130 million up from CHF 10.28 billion. Revenue from the sale of CO2 emission certificates decreased by CHF 6 million to CHF 4 million.

Holcim Leadership Journey

With total realized benefits of CHF 1.69 billion by the end of the third quarter 2014, Holcim already exceeded its operating profit objective of the Holcim Leadership Journey. The Group had committed to the target of a contribution to operating profit of CHF 1.5 billion by the end of 2014, compared to the base year 2011 and under similar market conditions. In the first nine months of 2014, the contribution of the Holcim Leadership Journey to the Group’s operating performance amounted to CHF 591 million. The Customer Excellence stream contributed CHF 214 million, and the cost initiatives CHF 377 million to this result.

Portfolio optimization in Europe

Holcim and Cemex announced on October 30, 2014 that they have agreed on adapted parameters to their series of transactions in Europe. In Germany and the Czech Republic, the scope of the transaction remains unchanged, meaning that Holcim will acquire Cemex’s operations in Western Germany while Cemex will take over Holcim’s business in the Czech Republic, as previously announced.

In Spain the two companies will no longer form a joint organization as initially planned and communicated. Instead, Cemex will purchase Holcim’s Gador cement plant and Yeles grinding station, with a total of 1.75 million tonnes of cement capacity, while Holcim will keep its remaining operations in Spain, representing 2.2 million tonnes of cement capacity, as well as its aggregates and ready-mix positions.

Due to the changed transaction, Cemex will pay Holcim EUR 45 million in cash. As a result of these changes, Holcim expects sustainable additional operating EBITDA of at least EUR 10 million on a yearly basis after the closing of the deal. These transactions are expected to close during the first quarter of 2015.

Merger between Holcim and Lafarge

On October 27, 2014 Holcim and Lafarge have formally notified the European Commission of their proposed merger in order to obtain regulatory approval. With this notification, Holcim and Lafarge have completed all necessary notifications with regulatory authorities worldwide. During the constructive pre-notification discussions which Holcim and Lafarge have had with the European Commission, the list of proposed assets for divestment was amended. In parallel to the regulatory process, Holcim and Lafarge have started the sales process and are in negotiations with potential buyers.

Outlook for 2014

For 2014 Holcim expects the global economies to show another year of uneven performance. Construction markets in Europe are expected to have reached the bottom with slow recovery in sight. At the same time, North American markets are expected to continue to benefit from a further recovery especially in the United States. Latin America on the other hand could continue to face uncertainties in Argentina but should overall show slight growth in 2014. The Asia Pacific region is expected to grow although at a comparatively slower pace than experienced in recent years. Africa Middle East is expected to gradually improve.

Holcim expects cement volumes to increase in all Group regions in 2014 with the exception of Europe. Despite positive development in North America, aggregates volumes are expected to decline. In ready-mix concrete volumes are expected to decline in all regions driven by restructuring and divestments.

The Board of Directors and Executive Committee expect that organic growth in operating profit can be achieved in 2014. The ongoing focus on the cost base coupled with all the benefits expected from the Holcim Leadership Journey will lead to a further expansion in operating margins in 2014.

Key figures per Group region

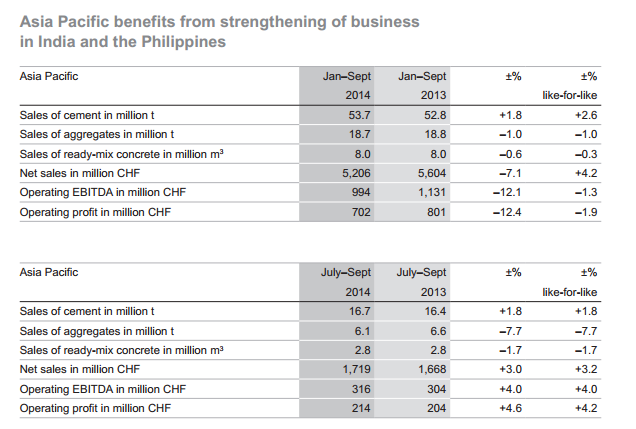

Asia Pacific benefits from strengthening of business in India and the Philippines

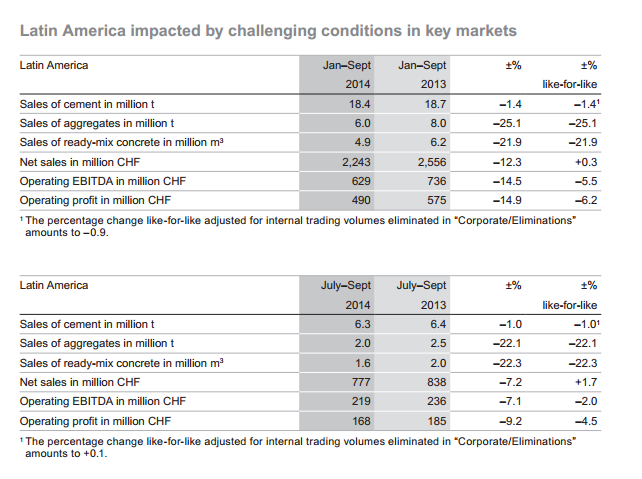

Latin America impacted by challenging conditions in key markets

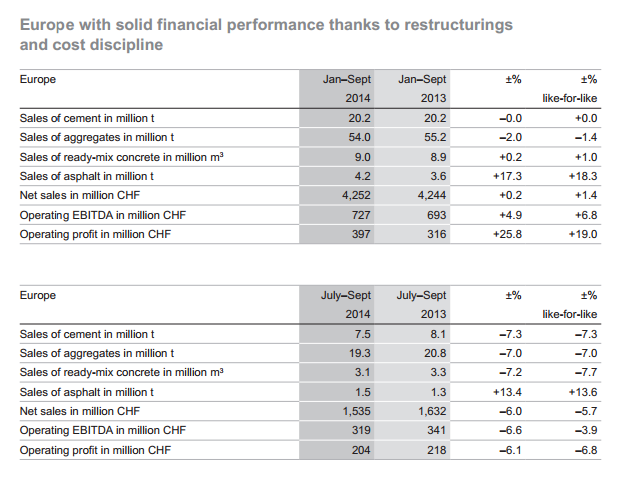

Europe with solid financial performance thanks to restructurings and cost discipline

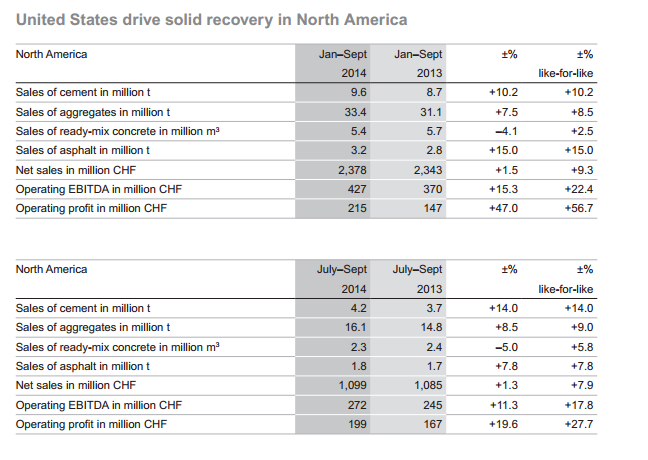

United States drive solid recovery in North America

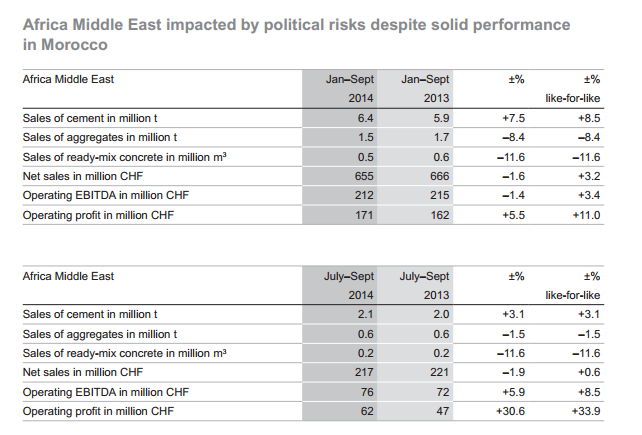

Africa Middle East impacted by political risks despite solid performance in Morocco

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Key figures Group Holcim, January-September

Additional information such as the 3rd Quarter Interim Report 2014 including detailed information on the Group regions is available at www.holcim.com/results

*****

Holcim is one of the world’s leading suppliers of cement and aggregates (crushed stone, gravel and sand) as well as further activities such as ready-mix concrete and asphalt including services. The Group holds majority and minority interests in around 70 countries on all continents.

*****

This media release is also available in German at www.holcim.com/news

*****

Corporate Communications: Phone +41 58 858 87 10

Investor Relations: Phone +41 58 858 87 87